Blockchain technology is revolutionizing banking by increasing speed and reducing costs. It eliminates intermediaries which significantly slashes operational costs. A report even estimated that big banks could save up to $10 billion by implementing blockchain in banking.

In addition, Blockchain in banking enhances efficiency and reduces transaction times by enabling direct peer-to-peer transfers, even for cross-border transactions. It also improves security, credit management, and risk assessment processes.

Keep reading to find out how blockchain in banking is challenging the status quo with faster, more cost-effective solutions.

The Banking Industry’s Current Challenges

Despite its vast potential, the banking industry currently grapples with several challenges, primarily its sluggish adaptation to the digital age, which results in operational inefficiencies, security vulnerabilities, and competition from the rapidly evolving fintech sector. Partnering with a financial technology provider can help banks overcome these challenges by offering advanced digital solutions.

Challenge 1: Struggling to Keep Up with Digital Shifts

Banks are having difficulty adapting to changes brought about by the tech age. Many of them still use old, manual ways that require piles of paperwork. This slows things down, increases the chance of mistakes, and opens doors to fraud.

To improve, banks must shift fully to digital, reinforcing blockchain in banking, making operations smoother and safer.

Challenge 2: Dealing with Cybersecurity

With the rise of online threats, banks can’t take the issue of security lightly. They need to use stronger, advanced ways to protect their customers’ information and transactions. Yet, a lot of banks still struggle to set up such safety systems. This puts pressure on them to tighten their security or risk losing the trust of their customers.

Challenge 3: Improving Credit Tracking

Traditional banks often find it hard to trace credit histories and manage bad credit. This flawed process could lead to monetary losses for the bank, harming its image and shaking customer confidence. Banks need a more efficient system to track and minimize bad credit.

Challenge 4: Facing Off with Rising Fintech Companies

Banks are facing more competition from fintech firms that use the latest technology to offer high-quality financial services. These innovative companies are quickly becoming more popular because they provide easy-to-use and efficient alternatives to the slow ways of traditional banks.

To stay in the game, banks need to speed up their use of technology, becoming more innovative and modernizing their services.

Blockchain: Revolutionizing Banking

Source

Blockchain technology offers solutions to many of the challenges that have plagued traditional banks.

These are the areas where blockchain in banking can bring improvements:

- the slow adaptation to the digital age,

- the inefficiencies resulting from reliance on paperwork,

- and the struggle to track credit history and reduce bad credits.

One of the benefits of blockchain in finance is its ability to modernize the banking sector, improving speed and efficiency in various activities. This technology reduces reliance on intermediaries, delivering significant cost savings.

Speeding Up the Move to Digital

Blockchain can assist banks in their shift to the digital world. This technology enables quick, in-the-moment transactions and updates. It can replace the old-school, paper-reliant ways that banks have been using.

Financial transactions can be easily recorded and reached on a blockchain system, cutting down on the time lost and mistakes made with paper processes. In this way, blockchain in banking helps banks speed up their move into the digital age, enhancing their overall efficiency.

Making Processes More Efficient

By using blockchain technology, banks can make their operations smoother and get rid of inefficiencies. Blockchain in banking cuts out the middleman in financial transactions, making transfers quicker and more straightforward. This not only speeds up and simplifies transactions but also saves a lot of money.

With blockchain in banking, banks can run in a more streamlined and cost-effective way.

Boosting Credit Tracking

With its shared, decentralized record of transactions, blockchain offers a clear and unchangeable log of credit histories. This allows for easier detection and management of bad credit, reducing the chances of financial loss. It not only reduces risk but also builds up trust and credibility with customers, strengthening the reputation of the bank.

Blockchain: A Game Changer in Cost Management

A 2017 report by Accenture suggests big banks could save up to $10 billion by implementing blockchain technology.

Blockchain’s decentralized nature is its biggest cost-saving attribute. It removes the need for third-party transaction verification, reducing both time and cost.

Banks often incur hefty fees for cross-border transactions due to multiple intermediaries. Blockchain in banking simplifies this, enabling direct peer-to-peer transfers that are both faster and cheaper.

Impact on Securities Trading and Credit Management

Blockchain in banking significantly improves trading securities. It does this by automating the process of confirming and settling trades, reducing the potential for mistakes and delays.

As a result, there’s less need for reconciliation — a process that can be costly.

In addition, blockchain advances the way credit is managed. Owing to its transparent nature, blockchain allows banks to track credit history effectively. This means fewer bad credits and loan defaults — issues that can be costly. Over time, these improvements can lead to major cost savings for the banks.

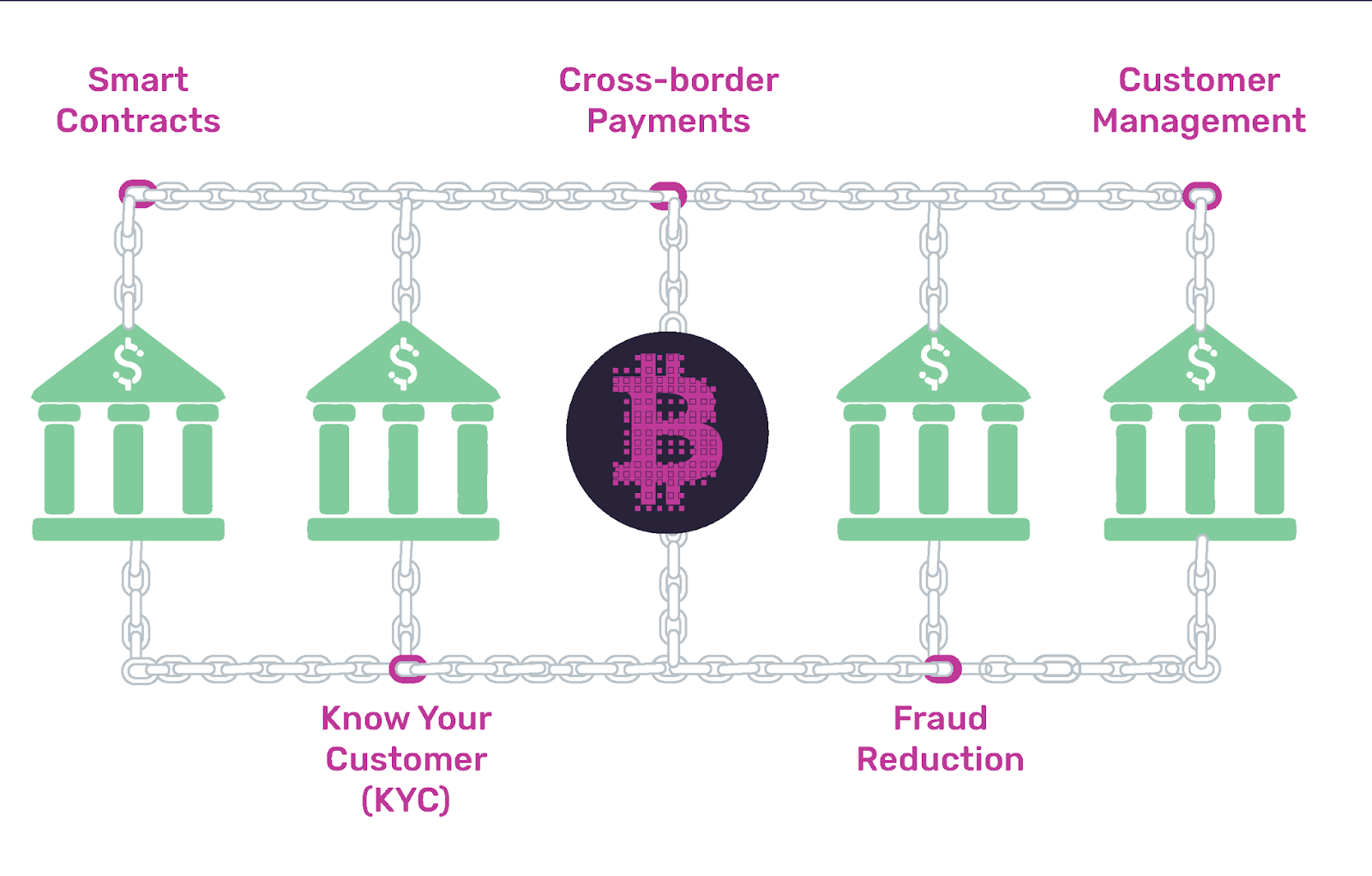

Practical Applications of Blockchain in Banking

Blockchain’s practical uses highlight its ability to make banking more efficient, safer, and more cost-effective.

- Quicker Transactions: Blockchain in banking can serve as an alternative settlement system, speeding up transactions. By removing the need for middlemen, it cuts down on both time and cost. This makes banking operations more efficient.

- Securing Digital Identity: Blockchain improves safety with digital identity checks. It provides secure verification processes, reducing the risk of fraud and identity theft.

- Peer-to-Peer Payments: Blockchain encourages payments to be made directly from one person to another, connecting parties and making money transfers easier. This cuts out the middleman, reducing costs and speeding up transactions.

- Safer Loans: Blockchain can make borrowing and lending safer and more transparent. With smart contracts, the terms and conditions can be automatically enforced. This lowers the risk of people not paying back loans and increases trust between everyone involved.

Optimizing Financial Transactions With Blockchain

With blockchain in banking, payments can be made instantly, overcoming issues like different time zones and work hours. This is helpful for international payments, which usually take several days to process. Thanks to blockchain, these payments can be completed in just a few minutes, no matter where the people involved are.

Simplifying Assets Transactions Through Tokenization

Another benefit of blockchain in banking is its ability to turn physical assets into digital ones and support digital currencies. This process, known as tokenizing, breaks down assets into smaller, easier-to-handle parts. This simplifies the process of buying, selling, and transferring assets.

The Future of the Banking Industry

Blockchain is quickly becoming a vital player in the banking world. Some even predict a future where the entire financial system runs on blockchain technology. This could offer an unparalleled level of efficiency and security that traditional systems just can’t compete with.

Blockchain’s Role in Security Enhancement

Source

Blockchain’s fortification of banking security not only deters cyber threats but also builds trust among users.

Decentralized System

Blockchain’s decentralized nature lowers the risk of data breaches. It disperses data across numerous points, each of which authenticates transactions. This means there’s no single weak point for hackers to target, making the system more secure.

Cryptographic Protection

Blockchain in banking further boosts security through encryption. Every transaction is encrypted and linked to the one before it, creating a chain of ‘blocks.’ Attempting to change information in one block would require changing every block that comes after it — a task that’s virtually impossible due to the amount of computing power needed.

Smart Contracts

The use of smart contracts in blockchain adds another safeguard. These self-executing contracts carry the terms of the agreement and automatically apply them. This reduces the chance of fraud or manipulation, making transactions safer and more trustworthy.

Conclusion

Blockchain in banking can make everything from transferring money to taking out loans easier, faster, and safer.

With its unique capabilities of cutting out middlemen, speeding up transactions, and providing rock-solid security, blockchain can step in and improve different aspects of banking.

Just think about a future where all banking tasks run on blockchain technology – it promises to be more secure, more efficient, and more cost-effective.

Frequently Asked Questions

How would blockchain technology reduce the costs of banking?

Blockchain can reduce banking costs by eliminating the need for intermediaries, reducing transaction times, and minimizing overhead costs. It allows for faster, more secure, and transparent transactions.

What are the benefits of blockchain technology in the banking sector?

In banking, blockchain technology enables faster and cheaper cross-border transactions, reduces fraud risks due to its transparency, and improves efficiency through smart contracts that automate various procedures.

What are the economic benefits of blockchain?

The economic benefits of blockchain include cost savings, improved efficiency, and greater transparency in various transactions. It can also enhance security, data integrity, and financial inclusion in the economy.

How does blockchain reduce cost?

Blockchain reduces costs by streamlining and automating traditional processes that regularly require third-party verification or time-consuming paperwork, like wire transfers, remittances, or contract enforcement.

How much money can blockchain save?

The amount of money blockchain can save varies across industries. For the banking sector specifically, a report by Accenture estimated that blockchain technology could reduce infrastructure costs by 30%, potentially saving banks $8-$12 billion annually.